CREDIT TIP: Regarding obtaining new credit (Part 1 – pros and cons to new credit)

There are a few things to be aware of if you are considering new credit.

Having open current (paid on time) credit is very important to having high credit score with all 3 credit bureaus (Equifax, Experian and TransUnion) . In fact, we have seen occasions where lack of open credit has prevented lenders from seeing any scores at all even though they can view the accounts on the report. We have seen occasions where clients have had all old closed positive credit and after cleaning off all or most of the derogatory accounts their scores still were only average due to lack of any current open credit.

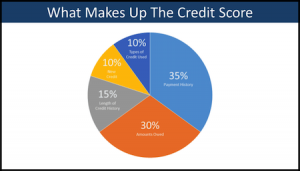

Another consideration is account variety. Account variety makes up 10% of your credit scores. It does help to have at least one installment type of loan (such as a mortgage, auto loan, student loan, etc) and at least one revolving account (like a secured or unsecured credit card). Secured credit benefits the credit score with all 3 credit bureaus (Equifax, Experian and TransUnion) in the same manner that unsecured credit does, but secured accounts tend to have additional fees (like higher interest rates or annual fees) due to the fact such accounts are designed for “riskier borrowers”. Secured credit is typically set up by putting money down and initially borrowing against yourself, but with the bank’s involvement to allow your ability to use the card to make purchases (and of course with their fees and interest).

When establishing new credit, the new account will lower scores for a few months. This is not due to any negative information, but is a result of lack of payment history. When an account is only a few months old it doesn’t have enough history for a potential lender to see how you really have managed the account. Once the account is six months old and shows a minimum of six months of on time (at least minimum) payments then the new account will begin to benefit the credit scores. For every additional month the account is active and paid on time the scores will continue to climb. Keep in mind that length of payment history makes up 15% of your credit scores. The longer your current accounts have been open and paid on time the better the scores can climb. Overall, establishing credit will be a good plan for your long term credit scores, but will hurt your scores for a few months. If you are planning to have credit checked for financing within the next few months and already have open credit it may make sense to wait.